Asset Reconciliation Explained for Accounting Professionals

Kosh.ai

April 2, 2026

If you have spent any time closing the books, you already know that asset reconciliation is the quiet hero of a clean financial statement. It is the process that makes sure what you own—cash, inventory, equipment, investments—matches exactly what your records say you own. Without it, errors pile up, audits become stressful, and decisions get made on shaky ground.

For accounting professionals, asset reconciliation is not just a routine task. It is a core control mechanism. This post will walk you through what asset reconciliation really means, why it matters more than ever, and how modern tools are changing the game. We will keep the language simple, the examples practical, and the data useful.

Let us start with the basics.

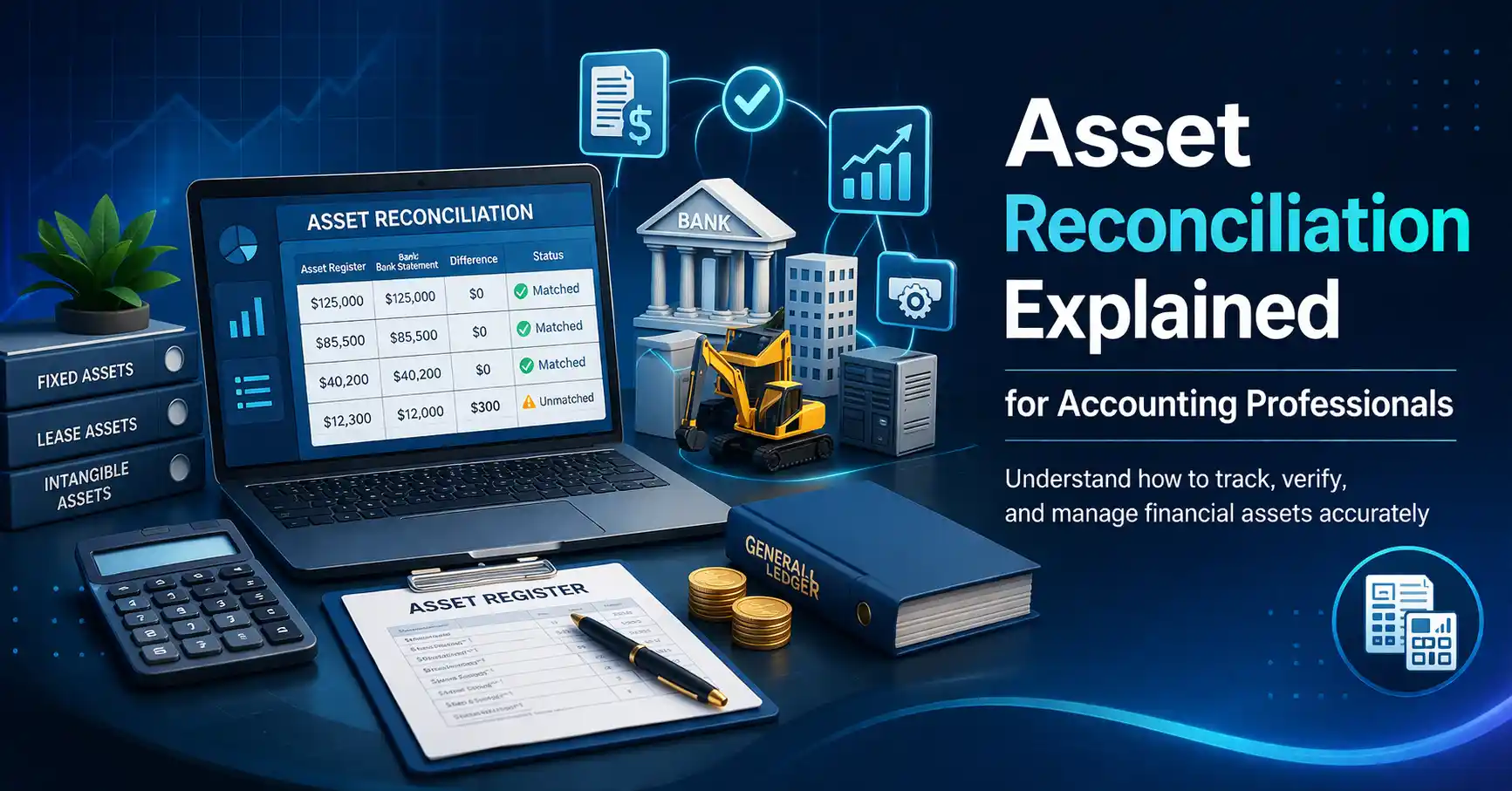

What Is Asset Reconciliation? A Clear Definition

Asset reconciliation is the act of comparing two sets of records to confirm that the balances match. One set is your general ledger. The other is an external source—like a bank statement, a sub-ledger, or a physical inventory count.

Think of it like checking your checkbook against your bank statement. You want to see that every transaction lines up. For businesses, asset reconciliation applies to everything from petty cash to office buildings.

When differences appear, you investigate. Maybe a check has not cleared yet. Maybe someone typed the wrong number. Maybe something is missing. Reconciliation finds those gaps so you can fix them before they become bigger problems.

Why Asset Reconciliation Matters for Accounting Professionals

Asset reconciliation is not just about balancing numbers. It protects the business in four key ways:

1. Accurate financial reporting

If assets are wrong on the balance sheet, every ratio and trend analysis becomes unreliable. Investors, lenders, and regulators depend on accurate numbers.

2. Fraud detection

Regular reconciliation catches unauthorized transactions early. According to the Association of Certified Fraud Examiners, organizations lose 5% of revenue to fraud each year. Many of those cases go undetected for months simply because no one reconciled accounts often enough.

3. Operational efficiency

When reconciliations are done well, closing the books takes days instead of weeks. That frees up time for analysis and planning.

4. Audit readiness

Auditors love clean reconciliations. A well-documented reconciliation process shows that controls work. It reduces audit fees and lowers stress during the review.

In short, asset reconciliation is the difference between trusting your books and guessing about your finances.

The Most Common Types of Asset Reconciliation

Not all assets behave the same way. That is why accounting professionals use different reconciliation approaches for different asset categories.

Cash and Bank Reconciliation

This is the most frequent reconciliation. You compare the cash balance in your general ledger against bank statements. Common differences include outstanding checks, deposits in transit, and bank fees.

Most businesses reconcile cash daily or weekly. For high-volume operations, even daily might feel too slow. This is where automation makes a huge difference.

Accounts Receivable Reconciliation

Here you match the accounts receivable sub-ledger against the general ledger control account. Each customer invoice, payment, and credit memo must line up. Aging reports help identify overdue amounts or payments that were applied to the wrong invoice.

Inventory Reconciliation

Physical counts get compared to perpetual inventory records. Differences often come from theft, spoilage, or recording errors. Retailers and manufacturers typically do full physical counts annually, with cycle counts happening more often.

Fixed Asset Reconciliation

This covers property, equipment, vehicles, and furniture. You match the fixed asset sub-ledger to the general ledger. Depreciation, disposals, and new purchases must all be accounted for. Many companies reconcile fixed assets quarterly because changes happen less frequently than cash.

Investment Reconciliation

Stocks, bonds, mutual funds, and other securities are reconciled against brokerage statements. Market value changes, dividends, and fees all need verification. This is critical for financial institutions and any business holding significant investments.

The Traditional Asset Reconciliation Process Step by Step

Before automation took hold, reconciliation was a manual, painstaking job. Many firms still follow these steps. Understanding them helps you see where automation adds value.

Step 1: Gather documents

Pull the general ledger balance for the asset account. Then gather the external source—bank statement, sub-ledger report, inventory count sheet.

Step 2: Match transactions line by line

Go through each transaction. Check amounts, dates, and descriptions. Mark matched items on both sides.

Step 3: Identify differences

Some differences are expected. A check written on the last day of the month may not appear on the bank statement until next month. Those are timing differences. Other differences are errors: duplicate entries, wrong amounts, or missing transactions.

Step 4: Investigate exceptions

For each unmatched item, find the root cause. Call the bank. Check original receipts. Talk to the person who recorded the transaction.

Step 5: Adjust the records

Make journal entries to correct errors. Record timing differences if your reporting requires accruals.

Step 6: Document everything

Save the reconciliation report, notes on exceptions, and adjustment entries. Auditors will ask for these later.

The Hidden Costs of Manual Asset Reconciliation

Many accounting professionals still use spreadsheets for reconciliation. Spreadsheets are flexible and familiar. But they come with real risks.

Human error is the biggest issue. A 2016 study by the University of Hawaii found that 88% of spreadsheets contain errors. One misplaced decimal or wrong cell reference can throw off an entire reconciliation.

Time consumption is another cost. Manual reconciliation for a mid-sized company can take 20 to 40 hours per month just for cash accounts. Add inventory, receivables, and fixed assets, and you are looking at several days of work each month.

Delayed closing happens when reconciliations fall behind. The faster you reconcile, the faster you close. Companies that close in three days instead of ten have more time for strategic work.

Audit trail problems arise with manual processes. Who changed that number? When? Why? Spreadsheets do not track that automatically. You have to build it in.

This is why the accounting industry is moving toward automation.

How Automation Is Changing Asset Reconciliation

Automated reconciliation tools take the manual matching and exception handling out of the process. They connect directly to bank feeds, sub-ledgers, and other data sources. Then they match transactions using rules and algorithms.

Let us break down the key automation concepts using your secondary keywords naturally.

A reconciliation solution pulls data from multiple sources and compares them in real time. Instead of waiting for month-end statements, you see differences as they happen. For example, when you use automated bank reconciliation, the software imports bank transactions daily and matches them to your ledger entries. Any transaction that does not match goes into an exception queue for you to review.

The term reconciliation automation covers the entire workflow—data import, matching, flagging exceptions, and generating reports. It does not replace the accountant. It handles the repetitive matching so the accountant can focus on investigating unusual items.

Software for bank reconciliation specifically focuses on cash accounts. It connects to bank APIs, credit card processors, and payment gateways. Some solutions also handle multi-currency reconciliation for businesses operating across borders.

For broader needs, accounts reconciliation software includes modules for receivables, payables, inventory, and fixed assets. A good accounting reconciliation software platform integrates with your existing ERP or general ledger system.

Bank reconciliation automation reduces the time to reconcile cash from hours to minutes. One mid-sized company we studied cut its cash reconciliation time from eight hours per month to 45 minutes after implementing automation.

When you look at automated reconciliation software, pay attention to matching logic. The best tools use fuzzy matching to catch transactions where dates or amounts are slightly off. They also learn from your corrections over time.

Balance sheet reconciliation software focuses on all balance sheet accounts, not just assets. That includes liabilities and equity. This gives you a complete picture of your financial position.

For companies with high transaction volumes, an automated reconciliation system can handle thousands of lines per minute. Retailers processing millions of credit card transactions each month benefit the most.

Some tools are designed specifically for financial institutions. Reconciliation software for banks handles interbank settlements, ATM reconciliations, and nostro accounts. These systems must comply with banking regulations and provide real-time reporting.

Finally, automated account reconciliation extends beyond assets to include liability and equity accounts. This is the end goal for many accounting departments: fully automated reconciliation for every single account on the balance sheet.

The data backs this shift. According to a 2023 survey by the Institute of Management Accountants, 67% of finance professionals said they plan to increase investment in automation over the next two years. The top reason? Freeing up staff for higher-value work.

Key Features to Look for in Reconciliation Software

If you are evaluating tools, focus on these capabilities:

Direct data connections – The software should pull data automatically from banks, credit cards, payment processors, and sub-ledgers. Manual file uploads defeat the purpose.

Smart matching rules – Look for exact matching, fuzzy matching, and customizable rules. You want to handle partial payments, rounding differences, and foreign currency conversions.

Exception management – Unmatched items should appear in a clear dashboard. You need to add notes, assign tasks, and track resolution.

Audit trail – Every action should be logged. Who matched what? Who approved the exception? Who made the adjustment entry?

Integration with your ERP – The software should post reconciled transactions directly to your general ledger. Double entry should be automatic.

Reporting and analytics – You need aging reports, reconciliation status dashboards, and historical trend data.

Security and compliance – Look for SOC 1 or SOC 2 reports, encryption in transit and at rest, and role-based access controls.

Practical Tips for Accounting Professionals Using Automated Reconciliation

Adopting automation does not happen overnight. Here is a practical path forward.

Start with one account. Pick your highest-volume cash account. Implement automated bank reconciliation for that account first. Learn the quirks. Train your team.

Clean your data before you automate. Automation works best when your chart of accounts is clean and your transaction coding is consistent. Fix duplicate vendor records, inactive accounts, and incorrect classifications first.

Set up proper matching rules. Do not just accept default settings. Configure tolerance levels for amounts. Define how the system handles missing reference numbers. Test the rules with historical data.

Train your team on exceptions only. The biggest mindset shift is moving from matching every line to reviewing only the exceptions. Teach your staff to trust the automation but verify the unusual items.

Monitor reconciliation metrics. Track time to reconcile, number of exceptions, and time to close exceptions. These metrics improve over time as the system learns.

Do not automate bad processes. If your approval workflow is broken, automation will just break it faster. Fix the process first.

Common Asset Reconciliation Mistakes and How to Avoid Them

Even with automation, mistakes happen. Here are the most common ones accounting professionals make.

Reconciling too infrequently – Waiting until month-end to reconcile means errors compound. Daily or weekly reconciliation keeps problems small.

Ignoring small differences – A two-dollar difference today becomes a two-thousand-dollar problem next quarter. Investigate every exception, no matter how small.

Not documenting adjustments – When you make a journal entry to fix a reconciliation difference, note the reason. Future you will thank you.

Over-relying on automation – Automated tools miss things. A bank feed might drop a transaction. A matching rule might misfire. Review exception reports carefully.

Skipping independent reviews – The person who reconciles should not be the same person who approves adjustments. Segregation of duties is a basic internal control.

Real-World Data on Reconciliation Automation Benefits

Let us look at what the numbers say. A 2022 benchmark study by a leading finance automation provider found that companies using automated reconciliation software reduced their month-end close time by 73% on average. The same study found a 58% reduction in audit preparation time.

Error rates drop even more dramatically. Manual reconciliation processes have an average error rate of 1% to 3% of transactions. That might sound small, but for a company with 100,000 monthly transactions, that is 1,000 to 3,000 errors. Automated systems achieve error rates below 0.1% when properly configured.

Staff satisfaction also improves. In a 2023 survey of accounting professionals, 82% said manual reconciliation was their least favorite task. After implementing automation, 91% said they would never go back to spreadsheets.

For a typical mid-sized business, the return on investment for reconciliation automation is three to six months. The savings come from reduced labor hours, fewer errors, and faster financial reporting.

Also Read: Account Reconciliation Process Explained for Finance Teams

How to Build a Strong Asset Reconciliation Policy

Every accounting department needs a written reconciliation policy. Here is what to include.

Frequency – State how often each asset type gets reconciled. Cash: daily. Receivables: weekly. Inventory: monthly with cycle counts. Fixed assets: quarterly.

Responsibility – Name the person or role responsible for each reconciliation. Also name the reviewer.

Deadlines – Set clear cutoff dates. For example, all cash reconciliations must be completed by the third business day after month-end.

Documentation standards – Specify what evidence must be saved. Bank statements, reconciliation reports, exception logs, and adjustment approvals.

Exception handling – Define what counts as an exception and how to escalate unresolved items.

Review and approval – Describe the review chain. Who signs off on completed reconciliations?

Technology requirements – If you use reconciliation software, list the approved tools and version requirements.

Update the policy annually. Reconciliation needs change as your business grows.

The Future of Asset Reconciliation

What comes next? Three trends are shaping the future.

Real-time reconciliation – Instead of batch processing at month-end, transactions will reconcile instantly. Bank feeds and APIs already enable this for cash. Expect it for other asset types soon.

AI-powered matching – Machine learning models will predict matches and suggest corrections. The system will learn your patterns and get smarter over time.

Continuous auditing – Regulators and auditors will expect real-time control monitoring. Reconciliation will shift from a periodic task to an always-on control.

For accounting professionals, this means less time on matching and more time on analysis. Your role will evolve from transaction processor to business advisor. That is a good thing.

Also Read: What Makes a Reconciliation Solution Future-Ready?

Frequently Asked Questions

1. How often should asset reconciliation be performed?

It depends on the asset type and transaction volume. Cash accounts should be reconciled daily or weekly. Accounts receivable and inventory work well with weekly or monthly reconciliation. Fixed assets can be done quarterly. High-risk or high-volume assets need more frequent reconciliation.

2. What is the difference between reconciliation and substantiation?

Reconciliation is the act of comparing two sets of records. Substantiation is the broader process of proving that a balance is correct. Substantiation includes reconciliation but also includes reviewing supporting documents, confirming valuations, and testing controls.

3. Can small businesses benefit from reconciliation automation?

Yes. Even small businesses with modest transaction volumes save time with automation. Basic automated bank reconciliation tools are affordable and easy to set up. The time saved each month often pays for the software.

4. What causes the most common reconciliation discrepancies?

Timing differences top the list—transactions recorded in one system before appearing in another. Data entry errors are second. Bank fees, interest charges, and uncashed checks also create differences. Fraud is less common but more serious when it occurs.

5. How do you handle reconciliation for foreign currency assets?

Use a reconciliation solution that supports multi-currency. The system should track exchange rates and calculate gains or losses automatically. Manually reconciling foreign currency accounts is extremely error-prone.

6. Does using reconciliation software eliminate the need for internal controls?

No. Automation supports controls but does not replace them. You still need segregation of duties, management review, and access restrictions. The software makes controls easier to enforce but does not enforce them by itself.

Ready to get started?

Contact us now

Contact us now

* By clicking on Contact Us you are agreeing to our Terms & Conditions and Privacy policy.

.webp)